Scilab 5.5.0

- Scilab Help

- Signal Processing

- filters

- analpf

- buttmag

- casc

- cheb1mag

- cheb2mag

- convol

- ell1mag

- eqfir

- eqiir

- faurre

- ffilt

- filter

- find_freq

- frmag

- fsfirlin

- group

- iir

- iirgroup

- iirlp

- kalm

- lev

- levin

- lindquist

- remez

- remezb

- srfaur

- srkf

- sskf

- syredi

- system

- trans

- wfir

- wiener

- wigner

- window

- yulewalk

- zpbutt

- zpch1

- zpch2

- zpell

Please note that the recommended version of Scilab is 2026.1.0. This page might be outdated.

See the recommended documentation of this function

lev

Yule-Walker equations (Levinson's algorithm)

Calling Sequence

[ar, sigma2, rc]=lev(r)

Arguments

- r

correlation coefficients

- ar

auto-Regressive model parameters

- sigma2

scale constant

- rc

reflection coefficients

Description

This function resolves the Yule-Walker equations using Levinson's algorithm. Generally, it is used to estimate the coefficients of an autoregressive process.

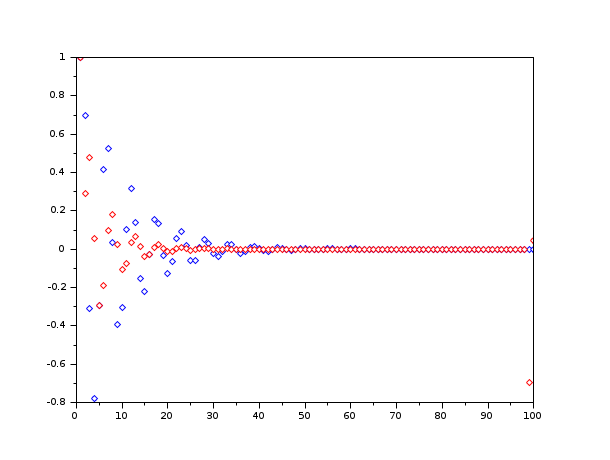

Example

b=1; //numerator a=[1 -0.7 0.8]; //denominator x=[1 zeros(1,99)]; //input=impulse data=filter(b,a,x); //real data a2=lev(data); //modelized data a2=a2/a2(1); //normalization m_data=filter(1,a2,x); // Compare real data and modelized data plot(data,"color","blue","lineStyle","none","marker","d"); plot(m_data,"color","red","lineStyle","none","marker","d");

| Report an issue | ||

| << kalm | filters | levin >> |