qld

linear quadratic programming solver

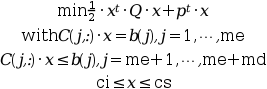

Syntax

[x [,lagr [,info]]] = qld(Q, p, C, b, ci, cs, me [,tol])

Arguments

- Q

real positive definite symmetric matrix (dimension

n x n).- p

real (column) vector (dimension

n)- C

real matrix (dimension

(me + md) x n)- b

RHS column vector (dimension

(me + md))- ci

column vector of lower-bounds (dimension

n). If there are no lower bound constraints, putci = []. If some components ofxare bounded from below, set the other (unconstrained) values ofcito a very large negative number (e.g.ci(j) = -number_properties('huge').- cs

column vector of upper-bounds. (Same remarks as above).

- me

number of equality constraints (i.e.

C(1:me,:)*x = b(1:me))- tol

Floating point number, required precision.

- x

optimal solution found.

- lagr

vector of Lagrange multipliers.

If lower and upper-bounds

ci, csare provided,lagrhasme + md + 2* ncomponents. The componentslagr(1:me + md)are associated with the linear constraints andlagr (me + md + 1 : 2 * n)are associated with the lower and upper bounds constraints.If an upper-bound (resp. lower-bound) constraint

iis activelagr(i)is > 0 (resp. <0). If no bounds are provided,lagrhas onlyme + mdcomponents.On successful termination, all values of

lagrwith respect to inequalities and bounds should be greater or equal to zero.- info

integer, return the execution status instead of sending errors.

info==1 : Too many iterations needed

info==2 : Accuracy insufficient to satisfy convergence criterion

info==5 : Length of working array is too short

info==10: The constraints are inconsistent

Description

This function requires Q to be positive definite,

if it is not the case, one may use the contributed toolbox "quapro".

Examples

//Find x in R^6 such that: //C1*x = b1 (3 equality constraints i.e me=3) C1= [1,-1,1,0,3,1; -1,0,-3,-4,5,6; 2,5,3,0,1,0]; b1=[1;2;3]; //C2*x <= b2 (2 inequality constraints i.e md=2) C2=[0,1,0,1,2,-1; -1,0,2,1,1,0]; b2=[-1;2.5]; //with x between ci and cs: ci=[-1000;-10000;0;-1000;-1000;-1000];cs=[10000;100;1.5;100;100;1000]; //and minimize 0.5*x'*Q*x + p'*x with p=[1;2;3;4;5;6]; Q=eye(6,6); //No initial point is given; C=[C1;C2]; b=[b1;b2]; me=3; [x,lagr]=qld(Q,p,C,b,ci,cs,me) //Only linear constraints (1 to 4) are active (lagr(1:6)=0):

See also

The contributed toolbox "quapro" may also be of interest, in

particular for singular Q.

Used Functions

ql0001.f in

modules/optimization/src/fortran/ql0001.f

| Report an issue | ||

| << optim | Optimization and Simulation | qp_solve >> |