qp_solve

linear quadratic programming solver builtin

Syntax

[x [,iact [,iter [,f [,info]]]]] = qp_solve(Q, p, C, b, me)

Arguments

- Q

real positive definite symmetric matrix (dimension

n x n).- p

real (column) vector (dimension

n)- C

real matrix (dimension

(me + md) x n). This matrix may be dense or sparse.- b

RHS column vector (dimension

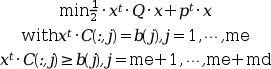

m=(me + md))- me

number of equality constraints (i.e.

x'*C(:,1:me) = b(1:me)')- x

optimal solution found.

- iact

vector, indicator of active constraints. The non zero entries give the index of the active constraints. The entries of the iact vector are ordered this way: equality constraints come first, then come the inequality constraints.

- iter

2x1 vector, first component gives the number of "main" iterations, the second one says how many constraints were deleted after they became active.

- info

integer, error flag. If it is present and qp_solve encounters an error, then a warning is issued. The current results are returned, so in this case they are probably inaccurate.

Description

This function requires Q to be symmetric positive

definite. If this hypothesis is not satisfied, one may use the contributed

quapro toolbox.

Examples

// Find x in R^6 such that: // x'*C1 = b1 (3 equality constraints i.e me=3) C1= [ 1,-1, 2; -1, 0, 5; 1,-3, 3; 0,-4, 0; 3, 5, 1; 1, 6, 0]; b1=[1;2;3]; // x'*C2 >= b2 (2 inequality constraints i.e md=2) C2= [ 0 ,1; -1, 0; 0,-2; -1,-1; -2,-1; 1, 0]; b2=[ 1;-2.5]; // and minimize 0.5*x'*Q*x - p'*x with p=[-1;-2;-3;-4;-5;-6]; Q=eye(6,6); me=3; [x,iact,iter,f]=qp_solve(Q,p,[C1 C2],[b1;b2],me) // Only linear constraints (1 to 4) are active

See also

- optim — non-linear optimization routine

- qld — linear quadratic programming solver

- qpsolve — linear quadratic programming solver

The contributed toolbox "quapro" may also be of interest, in

particular for singular Q.

Memory requirements

Let r be

r=min(m,n)

Then the memory required by qp_solve during the computations is

2*n+r*(r+5)/2 + 2*m +1

References

Goldfarb, D. and Idnani, A. (1982). "Dual and Primal-Dual Methods for Solving Strictly Convex Quadratic Programs", in J.P. Hennart (ed.), Numerical Analysis, Proceedings, Cocoyoc, Mexico 1981, Vol. 909 of Lecture Notes in Mathematics, Springer-Verlag, Berlin, pp. 226-239.

Goldfarb, D. and Idnani, A. (1983). "A numerically stable dual method for solving strictly convex quadratic programs", Mathematical Programming 27: 1-33.

QuadProg (Quadratic Programming Routines), Berwin A Turlach,http://www.maths.uwa.edu.au/~berwin/software/quadprog.html

Used Functions

qpgen2.f and >qpgen1.f (also named QP.solve.f) developed by Berwin A. Turlach according to the Goldfarb/Idnani algorithm

History

| Version | Description |

| 5.5.0 | Fifth output argument info added for error information. |

| Report an issue | ||

| << qld | Optimisation et Simulation | qpsolve >> |